As a small business owner and advisor, your attorney or accountant will provide many reasons why you should consider forming a corporation or limited liability company. These reasons include limiting personal liability, the ability to share equity, and possibly reduce taxes. For independent Registered Investment Advisory firms and insurance agencies, the setup and use of an entity is relatively routine – you file and form your business entity, and clients and/or carriers contract with that entity and pay that entity directly.

For independent registered representatives and those receiving income personally, on the other hand, this has proven more complicated to move revenue into the company, but not insurmountable with some upfront guidance. The recent Tax Court case of Fleischer v. Commissioner (TC Memo 2016-238) involving Mr. Ryan M. Fleischer, an Omaha, Nebraska advisor with LPL Financial Services, resulted in an uproar from advisors when Mr. Fleischer argued his case for using the corporation, only to lose and be forced to pay tens of thousands in back taxes.The Fleischer Case Background

Mr. Fleischer was a licensed registered representative with LPL (independent contractor) and an insurance agent with MassMutual (independent contractor), receiving 1099 income from both companies. Mr. Fleischer set up an S corporation in 2006 for his business purposes at the direction of his CPA. Due to licensing requirements, his broker-dealer would only pay him individually since he held the required securities license.

Once Mr. Fleischer received this income, he assigned it to his S corporation, Fleischer Wealth Plan, Inc. (“FWP”), where he was the sole shareholder and officer. He then contracted with himself as an employee of his corporation, paid himself a nominal salary of $35k in 2009 and took the balance out of net expenses as a distribution (thus paying less in taxes).

This process was repeated over the next two years as Mr. Fleischer continued to have success and grow his book of business. While his production grew to $266k in 2011, his salary from the corporation remained unchanged (resulting in a greater proportion of the revenue flowing out as distributions).

Mr. Fleischer was then audited in 2012 and spent the next four years arguing the merits of his strategy only to lose his case in 2016, being forced to pay $40k+ in back taxes.

The Court Case After the Audit

At first read of Mr. Fleischer’s case, one could assume that the use of an entity by an individually licensed registered representative was not permissible. However, there are numerous issues identified in the court documents related to this case that are important to understand in evaluating an advisor’s risk and developing best practices:

I. Assignability: Who is Assigned Revenue, the Individual or S Corp?

Issuance of compensation (and the ensuing 1099) to the individual and not the individual’s company (even if they have one) is a unique challenge for financial advisors since broker-dealers can only pay a licensed person. The Tax Court has indicated that the “issuance of Forms 1099 to the service provider and not the corporation…are almost always dispositive in favor of Commissioner.”[1]

In other words, income is taxed to the person who earned it. This long-standing tax principal is intended to prevent people from assigning their income elsewhere and avoiding taxation. The key here is to ensure that there is a business purpose and agreement for moving the revenue into the company, and that the purpose is not for tax avoidance.

Despite the employment agreement between Fleischer and FWP, Fleischer had no contractual obligation to pay his revenue to FWP, nor did he have an agreement between FWP and its clients or with LPL and MassMutual. The Tax Court therefore determined that Mr. Fleischer is unable to assign the revenue he earned as an advisor to his S corporation, FWP. This is unfortunate for advisors like Mr. Fleischer who are required to receive compensation from their broker-dealer personally under FINRA’s Rule 2040.

II. Reasonable Compensation with an S Corp

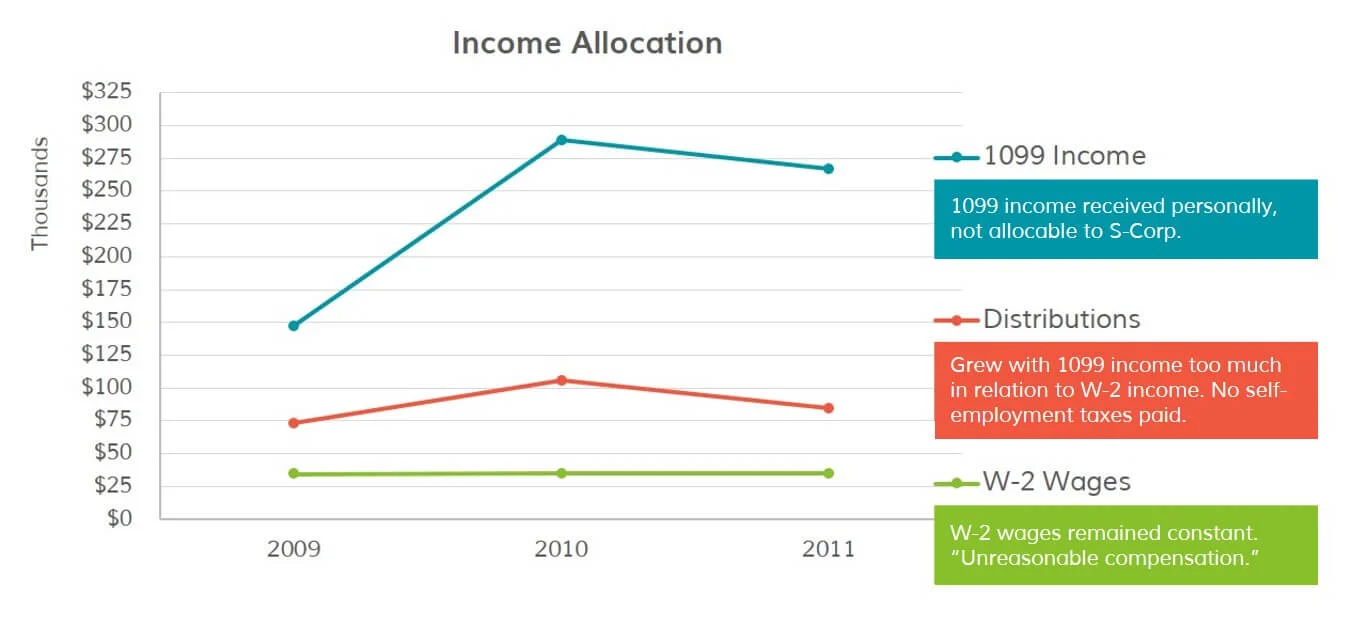

Mr. Fleischer’s W-2 wages from his S corporation were consistently $35k, with distributions upwards of $74k, as shown in the table below. Not only is this inconsistent based on the 1099 income he received, but it is also a low salary for an individual in his role and in his industry. Similarly, the distributions are significantly skewed to his benefit, as no self-employment taxes are paid on distributions.

When using a corporation as the entity structure of choice, you can distribute income to the owners in the form of profit distributions at a more tax advantaged rate than normal earned income. Because of this bifurcation of income and ability to pay less taxes, it is critical to ensure owners pay themselves reasonable compensation.

III. Does the Advisor Control of the Money?

To establish who earns the income, the Tax Court determines whether the individual or his/her company controls the earning of the income. As a result, the court applies the following two-part test which is required to be met before the corporation (not the individual) is deemed to control the earnings:

1. Corporation’s Control of Employer/Advisor

The individual must be an employee of the corporation, which must have the right to direct or control the employee in some meaningful sense.

While Mr. Fleischer did execute an employment agreement between FWP and himself, it did not appear to the court that there was sufficient evidence that FWP had any control over Mr. Fleischer, particularly since Mr. Fleischer has maintained complete control over FWP. The court indicated that the employment agreement was too “generic” and did not reference specific language allowing FWP to assert control over or economic substance over Fleischer or the revenue he was assigning at his discretion.

2. Corporation’s Control of Earning of Income

There must be a contract or similar arrangement between the corporation and the person/entity using the services, which recognizes the corporation’s right to direct or control the work of the individual.

IRC Section 482 describes this in more detail, indicating that this code section is used to determine taxable income and to “ascertain whether common control is being used to reduce, avoid, or escape taxes.”[2] In the case of Fleischer, Mr. Fleischer set up FWP as an S corporation, but was also the sole owner of FWP, the sole employee of FWP, and the president, secretary, and treasurer of FWP.

According to the Tax Court documents, FWP “has never entered into any agreements or contracts with any other third-parties.”[1] This statement implies that all contracts under the umbrella of FWP (employees, CPAs, attorneys, utilities, rental agreements, etc.) were conducted personally and outside Fleischer’s position as CEO of FWP. Mr. Fleischer also failed to notify LPL Financial and MassMutual that he was also an employee controlled by his corporation[3].

By not acting in his capacity as an employee or officer of the company, and having agreements signed personally but paid by the corporation, the IRS’s position was reasonable that the individual (Mr. Fleischer), not the corporation (FWP), was the true earner of income. This was compounded by the fact that Mr. Fleischer indicated that he could have had the corporation enter into an agreement with MassMutual, but chose to do it personally.

Will Using an LLC or S Corp Trigger an Audit?

With much to learn from Fleischer v. Commissioner, a question financial advisors are asking at this point is, “Can I use an LLC or corporation, and if I do, am I at an increased audit risk?”

Yes, you can use an LLC or S corporation even as someone receiving compensation directly from a broker-dealer (unless the broker-dealer prohibits you), but your risk of an IRS audit depends on how conservative or aggressive you and your tax counsel choose to be.

It is also important to know that Fleischer v. Commissioner did not change tax law, but merely reiterated what has already been in place. So, what can we take away from the case?

First, independent Registered Investment Advisory (RIA) firms that are structured as a corporation are not at an increased audit risk. RIA firms are not required to be registered with a broker-dealer and can have their advisory clients engage directly with the RIA,[4] thus eliminating the assignment and control of income issues.

Second, limited liability companies (LLCs) taxed as a sole proprietorship or partnership will likely also have no issues, as all income generated flows directly to their individual owners’ returns and self-employment taxes are paid. This leaves registered representatives using a corporation.

In the following section, we show the two best ways to use your entity to reduce the likelihood of an audit and an ensuing tax bill, depending on how aggressive or conservative you and your CPA choose to be.

SRG Guidance for Financial Advisors

There are many important reasons to set up and use an LLC or corporation even as a registered representative, such as limited personal liability and easy transfer of ownership interest. The downside is that if you receive revenue from a broker-dealer and subsequently move that money to an entity, particularly S corporations, you are at an increased risk of an IRS audit.

The keys to success? Understand the two best practices (and the important steps related to each strategy) advisors should use effectively:

1. An agreement where you contract with your entity for services

OR

2. An agreement where you are employed by the entity with a requirement to assign revenue

It is important to have the right agreements in place for your industry, be well documented in a corporate capacity and have reasonable compensation for employee/owners. The Fleischer case provides a specific example of how the existing tax laws can be applied to the financial industry. It implies that your current structure might not be bullet proof. There is added risk if you are going to proceed as a corporation and assign your revenue to an S corporation, in which case you should consult your tax advisor.

The most conservative approach for financial advisors is to operate as an LLC (Schedule C filing), rather than an S corporation. This approach still affords the extra layer of personal liability protection and allows you to easily share equity, but also results in paying self-employment tax, which appears to be the primary issue in this case.

If using a corporation is desired and advised by your accountant, consider employing the more conservative solution – contracting with your company for services and do not put yourself on payroll. If assigning the revenue and acting as an employee of your business is preferable, ensure you are well counseled and follow all the industry specific best practices to avoid issues.

Final Thoughts on the Fleischer Tax Case

With this recent tax ruling involving the LPL advisor, we now have a specific example of how the tax law could be applied to your industry, but it is important to understand the nuances of this case. If you have your ‘ducks in a row’ and your tax counsel well advised by an industry consulting firm (such as Succession Resource Group), you will be in a much better position than Mr. Fleischer in the event the IRS pays you a visit.

We hope that this article will help you avoid the same fate.

Explore other Entity and Employment content

About Succession Resource Group

Based in Portland, Oregon, Succession Resource Group, Inc. is a boutique consulting firm committed to helping financial advisors with their acquisition and succession needs. Founded and led by David Grau Jr., MBA, a succession planning consultant for more than a decade working with financial professionals, SRG provides turnkey customized acquisition and succession planning solutions nationwide, helping both individuals as well as providing firm-wide solutions for broker-dealers and custodians. SRG’s suite of services includes business valuation, business structuring and equity compensation strategies, talent development, contingency planning, acquisition support, deal support (including personal consulting, deal structuring, tax strategies, checklists, transition packet, and comprehensive customizable form contracts), succession planning, and personalized consulting.

[1] https://www.ustaxcourt.gov/UstcInOp/OpinionViewer.aspx?ID=11057

[2] https://www.irs.gov/irm/part4/irm_04-011-005.html

[3] https://www.currentfederaltaxdevelopments.com/blog/2016/12/29/income-earned-by-financial-adviser-and-not-s-corporation-net-earnings-subject-to-self-employment-tax

[4] https://www.kitces.com/blog/meeting-the-requirements-to-start-your-own-ria-without-breaking-the-bank/